Indiana Car Accident Claim Calculator: 2026 Settlement Guide

Indiana Car Accident Lawyer

Indiana Car Accident Claim Calculator: 2026 Settlement Guide

The crash is over, but the uncertainty starts fast. Your car may be in the shop. Medical bills are arriving. You've missed work, and the adjuster wants a statement before you've had time to think clearly.

So you search for a car accident claim calculator.

A box asks for medical bills, lost wages, maybe a pain-and-suffering multiplier. You click a button and get a number that feels like relief. For a moment, it seems like someone has translated your disruption, pain, and financial stress into something concrete.

That's why these calculators are popular. They offer certainty when your life suddenly has very little of it.

The problem is that many of them are built for a generic claim, not an Indiana claim. They can help you understand the rough pieces of a case. They usually cannot tell you what your case is worth. In Indiana, fault allocation, available coverage, and the evidence behind your injuries can change the number sharply. In some cases, they can wipe it out completely.

The Alluring Promise of an Instant Settlement Figure

A typical post-accident search goes like this. You type in your expenses, choose a multiplier that sounds reasonable, and a website produces a surprisingly large estimate. If you're hurting and worried about money, that result can feel like validation.

That reaction makes sense. A calculator gives structure to a messy situation.

But the number on the screen is usually closer to a rough classroom exercise than a real settlement evaluation. It's based on a simplified formula, often without asking the questions that decide real Indiana cases. It won't know whether the insurer is disputing liability, whether your treatment records support the symptoms you describe, or whether some share of fault may be assigned to you.

Why the estimate feels persuasive

Most calculators are designed to be simple. That simplicity is the appeal. You enter a few costs, pick an injury severity level, and get a result in seconds.

The catch is that speed comes from omission. The form leaves out the hard parts.

A quick estimate can be a useful starting point. It becomes dangerous when someone treats it like a settlement guarantee.

A good evaluation doesn't start and end with arithmetic. It asks different questions:

- What can you prove: Bills matter, but so do diagnosis, treatment history, and whether the records tie your condition to the crash.

- Who will be blamed: In Indiana, the fault question isn't a side issue. It can control the outcome.

- What coverage exists: A claim may be worth more on paper than what's realistically collectible.

- How will the insurer value the file: Insurance companies don't rely on your online calculator.

What the tool still gets right

A car accident claim calculator can help you organize your thinking. It can remind you to gather wage loss information, repair documents, and medical records. That's useful.

It just can't replace a state-specific legal analysis. For Hoosiers, that distinction matters more than is often realized.

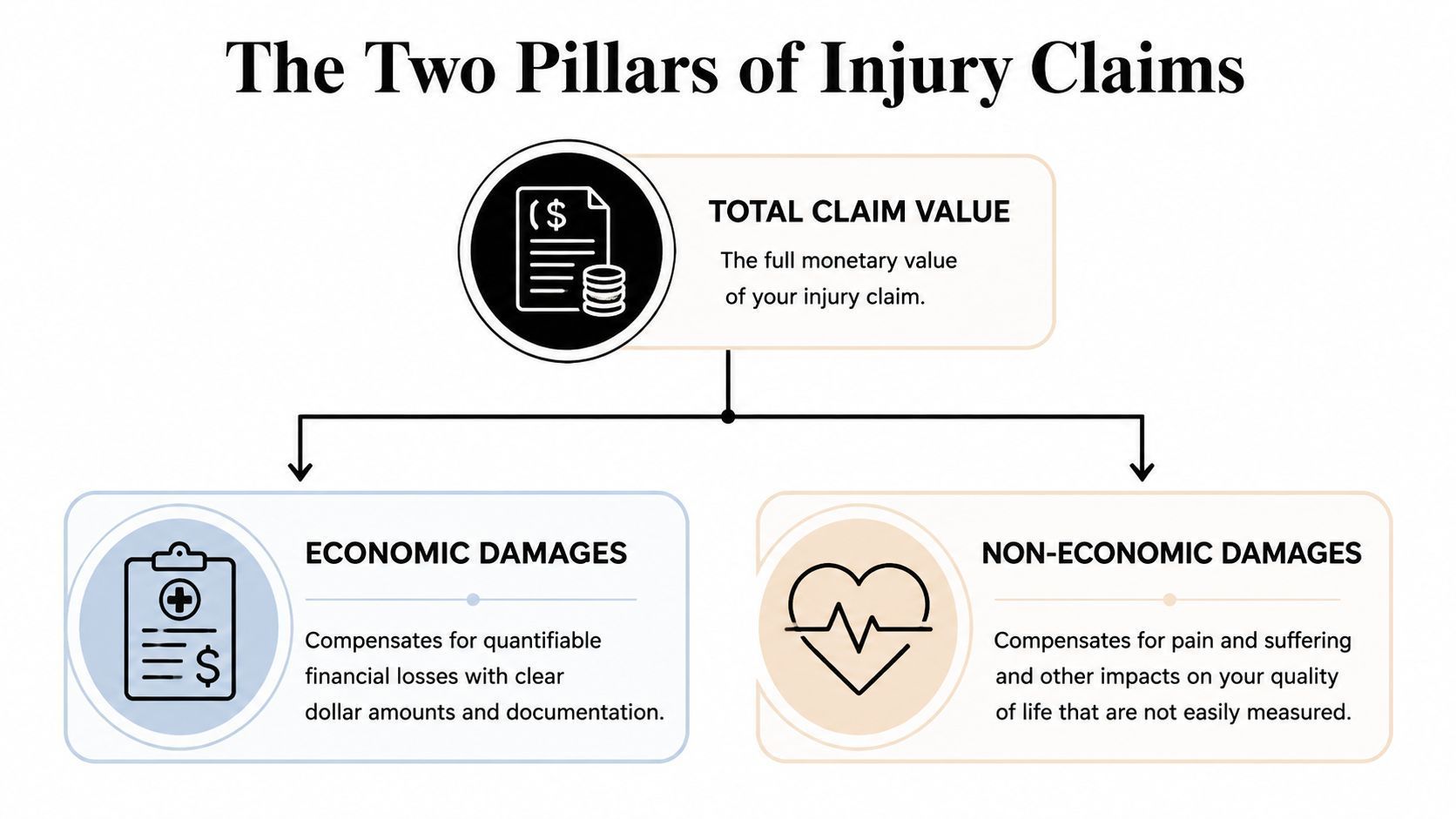

Deconstructing a Claim What Calculators Ask For

Every injury claim starts with two broad categories of damages. If you don't understand those categories, the calculator's inputs look arbitrary. If you do understand them, you can spot where the estimate starts drifting away from reality.

Economic damages

These are the financial losses you can document. Think of them as the receipts side of the case.

Common examples include:

- Medical expenses: Emergency care, follow-up visits, physical therapy, imaging, prescriptions, and other treatment tied to the crash.

- Lost income: Pay you missed because your injuries kept you from working.

- Property damage: Repair or replacement costs for your vehicle and damaged personal property.

These numbers form the base of most calculators. They're the easiest part to enter because they come from bills, pay records, and repair estimates. If you're dealing with an injury claim after an Indiana wreck, the practical starting point is gathering the same categories that appear in a standard Indiana car accident case evaluation.

Non-economic damages

This category covers the human impact of the collision. It includes pain, physical limitations, disruption to daily life, and the emotional strain that comes with injury.

These losses are real, but they don't come with invoices. That's why calculators struggle with them.

A sore neck that resolves quickly is different from a back injury that affects sleep, work, driving, and family responsibilities for months. A calculator can ask you to choose “minor,” “moderate,” or “severe,” but those labels are blunt tools for a very personal experience.

Why calculators ask for a multiplier

Most online tools use the multiplier method, which became a standardized approach in personal injury litigation during the mid-20th century and was widely adopted by U.S. insurance adjusters and attorneys by the 1980s. Under that method, total economic damages are multiplied by a factor usually ranging from 1.5 to 5 to estimate pain and suffering, as described by this explanation of the multiplier method.

That framework is easy to understand. It's also where subjectivity enters the process.

Practical rule: The bills are only the beginning. The real dispute usually centers on how serious the injury is, how long it lasted, and how convincingly the records support it.

A calculator can capture the categories. It usually can't judge the strength of the proof behind them.

The Math Behind the Estimate Common Calculation Methods

Most settlement estimates come from one of three approaches. Two are simple enough for public calculators. The third is what many insurers use behind the scenes.

The multiplier method

This is the engine behind most car accident claim calculator tools. The basic idea is straightforward. Add up the economic damages, then apply a multiplier that reflects injury severity.

The friction is in choosing the multiplier.

A minor soft-tissue case may draw a lower number. A claim involving surgery, permanent symptoms, or serious disruption to daily life may justify a higher one. The formula looks objective, but the multiplier itself is where adjusters and claimants often disagree. One side sees a temporary strain. The other sees months of treatment, interrupted work, and daily pain.

That disagreement is why two people can input the same bills and reach very different estimates.

The per diem method

Some lawyers and adjusters also use a per diem approach. Instead of multiplying losses, they assign a daily value to the period of pain and limitation.

This method can help frame short, clearly defined recovery periods. It becomes harder to use when symptoms fluctuate, treatment is ongoing, or the recovery timeline isn't clean. That's why many online calculators don't lean on it heavily. It requires judgment calls the software can't make well.

The insurer's internal software

Insurance companies often don't evaluate claims the way public calculators do. Many use proprietary systems built to standardize injury valuation. One well-known example is Colossus.

According to Miller & Zois on Colossus, the software uses around 600 standardized injury codes and over 10,000 rules to calculate claim values. It also looks at the plaintiff attorney's litigation history, and an attorney known for trying cases against low offers can affect projected value by 20 to 50 percent.

That matters for two reasons.

First, insurers aren't just reading your medical bills and picking a number out of the air. They're entering information into structured systems that reward certain documentation and discount weak or incomplete files.

Second, the reputation of counsel can change the insurer's risk analysis. If the carrier believes a low offer will likely be accepted, the valuation pressure is different from a file attached to a lawyer with a trial record.

What works and what doesn't

A simple formula works best when liability is clear, treatment is consistent, and the records tell a clean story. It works poorly when there are treatment gaps, preexisting issues, disputed fault, or insurance coverage problems.

Here's the practical trade-off:

- Calculators help with orientation: They teach you what categories matter.

- They fail at valuation: They can't judge credibility, proof, venue, or negotiation pressure.

- Insurance software is not neutral: It standardizes claims, but standardization can flatten the lived reality of an injury.

The most important number in a calculator is often the one the user guesses. That's the multiplier. Guess wrong, and the whole estimate tilts with it.

How Indiana Law Changes the Entire Equation

Indiana law doesn't just tweak a settlement estimate. It can change it.

Indiana comparative fault

The biggest issue most generic calculators miss is Indiana's modified comparative negligence rule. Under IC 34-51-2-6, a claimant recovers nothing if they are found 51% or more at fault, and research discussing calculator gaps in Indiana notes that 28% of auto claims in Indiana court records from 2023 to 2025 were reduced by this type of fault apportionment.

That's not a minor adjustment. It's often the central fight in the case.

A generic calculator might ask whether you were “partially at fault,” but that's not enough. Indiana requires a precise legal analysis of how fault may be assigned and whether your percentage falls below or above the line. A rough national tool can't make that call.

For a more personalized discussion of how liability and damages interact under Indiana law, a focused Indiana personal injury settlement review is far more useful than a one-size-fits-all calculator.

Why fault disputes grow quickly

Clients often think fault is obvious. Sometimes it is. Sometimes it isn't.

Rear-end cases can involve sudden stopping arguments. Intersection crashes can turn on signal timing, witness credibility, and whether one driver was speeding. Lane-change collisions raise disputes about blind spots, signaling, and positioning. Once the insurer sees room to assign part of the blame to you, the calculator's tidy number starts to unravel.

That's especially true when digital evidence exists, police narratives are incomplete, or the injuries themselves lead the carrier to contest how much of the treatment was really caused by the crash.

Indiana and medical payment issues

People also confuse settlement value with what gets paid along the way. Indiana is not a no-fault state, and generic online discussions about “PIP rules” often mislead Hoosiers because they blend concepts from other states into one national formula.

What matters in practice is whether there is available medical payments coverage, how bills are being handled while the claim is pending, and whether your own coverage or health insurance is filling the gap. A calculator usually doesn't ask any of that. It assumes the math exists in a vacuum, when in reality the way treatment is paid and documented can affect the claim's momentum and presentation.

Deadlines matter more than estimates

Another issue calculators ignore is timing. Indiana injury claims are governed by filing deadlines. If you miss the deadline, the quality of your medical records and the size of your losses won't rescue the claim.

That's one of the biggest differences between a legal evaluation and a calculator output. A lawyer looks at recoverability. A calculator only performs arithmetic.

A practical Indiana checklist

When evaluating an Indiana crash claim, ask these questions early:

- How will fault be argued: This can reduce recovery or eliminate it.

- What records support the injuries: Consistent treatment matters.

- What coverage is available: The paper value of a claim isn't always the collectible value.

- What deadlines apply: A strong claim still has to be filed on time.

A Tale of Two Claims A Sample Indiana Calculation

A sample shows the problem better than an abstract warning.

Assume an injured driver has documented economic damages. A generic car accident claim calculator applies a multiplier and produces a promising figure. Then Indiana fault rules enter the picture.

Step one, the broad estimate

Using a standard multiplier approach, the calculation starts with economic losses and adds non-economic damages based on injury severity. That's the familiar online process.

The reason that number can change so sharply is comparative fault. By 2026, 46 states are projected to use some form of comparative negligence, and in modified-fault states like Indiana, being over 50% at fault bars recovery. One cited example shows a $94,000 claim reduced to $75,200 when the claimant is 20% at fault, as explained in this discussion of comparative negligence and calculators.

That example captures the core point. The same damages can produce very different outcomes depending on fault allocation.

Step two, the Indiana adjustment

Below is a simple illustration of how that plays out in practice. The exact starting amount is hypothetical, but the legal effect of fault is the part that matters.

Calculation Step Scenario A (20% At Fault) Scenario B (51% At Fault) Initial calculator estimate Same starting estimate Same starting estimate Indiana comparative fault applied Reduced by claimant's share of fault Recovery barred Result Claim value is cut down Claim value becomes zero This is why people get frustrated when the insurance offer is nowhere near the online estimate. The calculator gave them a national-style projection. Indiana law imposed a legal filter the tool never really analyzed.

The lesson from the comparison

Two claims can begin with nearly identical medical bills and wage loss. One settles because the injured person's fault stays low enough to preserve recovery. The other collapses because the evidence pushes fault beyond the Indiana threshold.

That's not a flaw in arithmetic. It's the legal reality of the case.

If liability is being contested, the most important part of your claim may not be the damage total. It may be the evidence that keeps your fault percentage below the line.

A calculator is most useful when fault is clear and the injuries are straightforward. It becomes less reliable as soon as the case turns into an argument about who caused what. In Indiana, that argument often determines whether the numbers matter at all.

The Hidden Factors Online Calculators Never Ask About

Even a better-than-average calculator leaves out variables that experienced adjusters and attorneys look at immediately.

Policy limits

The calculator may tell you what the injury seems worth in theory. It does not tell you what money is available.

If the at-fault driver carries limited insurance, that can place a practical ceiling on recovery unless other coverage applies. This is one of the first things lawyers investigate and one of the last things most consumers think about when they're using an online tool.

Telematics and black box evidence

This issue has become more important, not less. Since Q1 2025, Indiana insurers have increasingly used vehicle telematics and AI dashcam analysis for fault determination, contributing to a 35% rise in data-driven denials nationwide. The same analysis states that calculators may undervalue claims by 20% to 40% because they can't account for black box or tracking-app data, according to this review of telematics and settlement calculators.

That means your claim may be shaped by information you never entered into the calculator and may not even know exists yet.

For anyone sorting through evidence after a crash, a practical guide on what to do after a car accident can help preserve the details that matter before the insurer frames the story first.

The lawyer factor

This surprises people, but it's real. Insurers evaluate not just the injuries and bills, but the likely path of the case.

If the carrier believes the claim will be pushed hard, documented thoroughly, and prepared for litigation, the negotiation posture changes. If the file looks like it will settle cheaply, the pressure goes in the opposite direction. No public calculator asks who is presenting the claim, how the records are organized, or whether the insurer expects trial risk.

Questions the calculator never asks

- What if your records show treatment gaps: The insurer may use them to argue the injury wasn't serious.

- What if the vehicle data conflicts with your account: Fault may shift.

- What if coverage is limited: The value on paper may exceed the money available.

- What if the defense expects no lawsuit: The opening offer may reflect that assumption.

A calculator is a clean, closed system. Real claims are not.

When to Stop Calculating and Contact an Attorney

Use a car accident claim calculator for orientation, not decision-making. It can help you identify categories of loss and gather documents. It cannot tell you whether your fault percentage puts recovery at risk, whether the insurer has a hidden advantage from digital vehicle data, or whether the available coverage supports the number on the screen.

That difference matters most when any of the following are true:

- Liability is disputed

- You have more than minor injuries

- You missed work

- The insurer is questioning treatment

- You're being blamed for part of the crash

- You're close to a filing deadline

A real claim evaluation is part law, part evidence, part negotiation strategy. Generic calculators only handle the first layer of the math, and even that is usually incomplete for Indiana cases.

The right time to stop plugging numbers into a website is when you need an answer you can act on.

If you were hurt in an Indiana crash and want a real case assessment instead of a generic estimate, contact the Law Office of Mark Nicholson. You can discuss the facts of your accident, how Indiana fault rules apply, and what your claim may be worth in a free, no-obligation consultation.